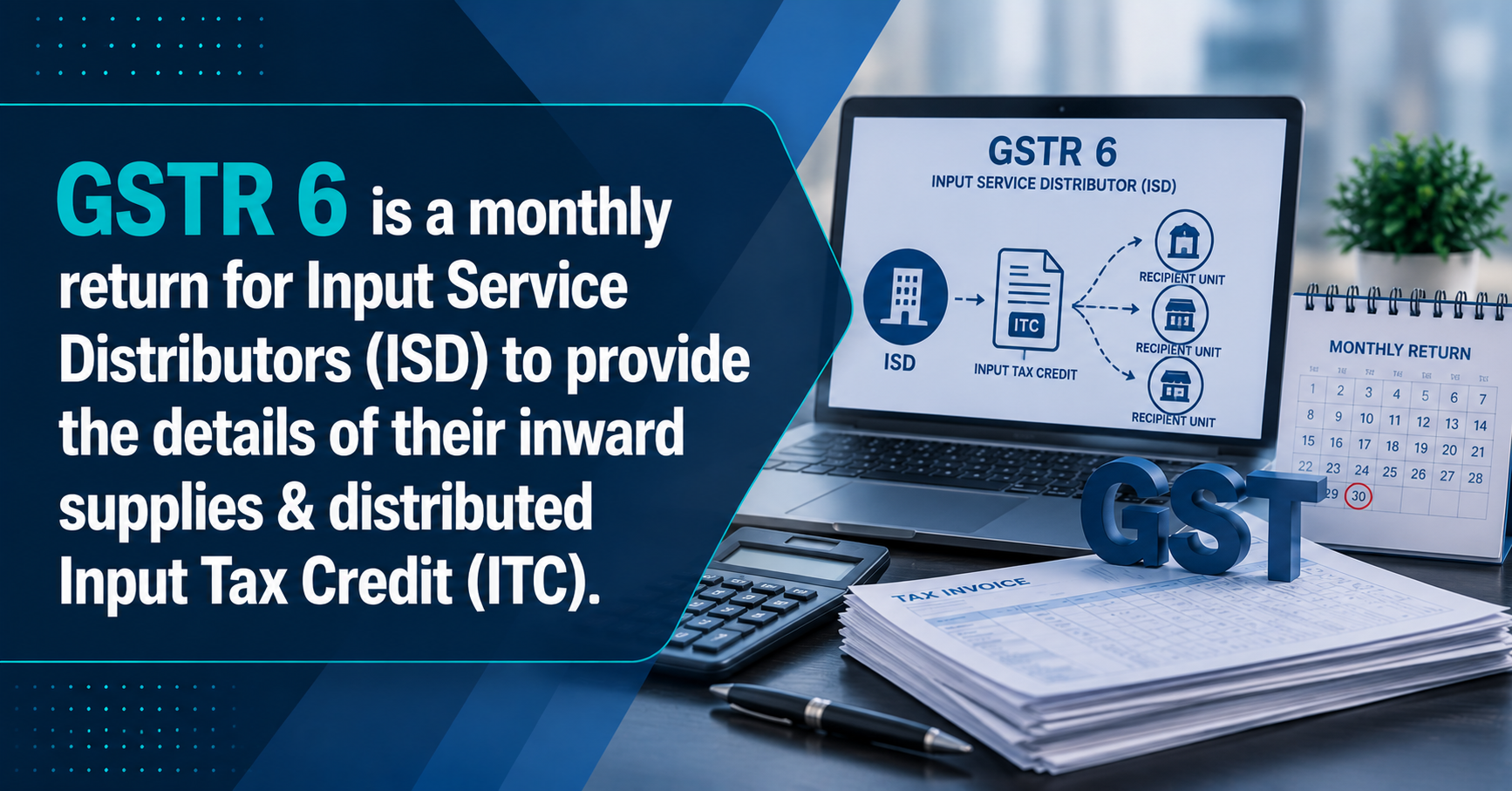

Upcoming Deadline: GSTR 6 is a monthly return for Input Service Distributors (ISD) to provide the details of their inward supplies & distributed Input Tax Credit (ITC). — Due 13 May 2026

GSTR-6 is a monthly GST return required to be filed by Input Service Distributors (ISD) for reporting inward supplies and distribution of Input Tax Credit (ITC) to branches or units registered under the same PAN.

Proper filing of GSTR-6 is important for accurate ITC allocation and GST compliance across multiple business locations.

What is GSTR-6?

GSTR-6 is a monthly return filed by an Input Service Distributor under the GST regime.

The return contains details relating to:

- Inward supplies received by the ISD,

- Input Tax Credit available,

- Distribution of ITC to recipient branches or units,

- Credit notes and debit notes received from suppliers.

The return is filed electronically on the GST portal.

Who is an Input Service Distributor (ISD)?

As per Section 2(61) of the Central Goods and Services Tax Act, 2017:

An Input Service Distributor is an office of the supplier which receives tax invoices for input services and distributes the eligible ITC to distinct persons having the same PAN.

Typically, head offices receiving common service invoices for multiple branches register as ISDs.

Legal Provisions Governing GSTR-6

The filing of GSTR-6 is governed by:

- Section 39 of the CGST Act, 2017;

- Rule 65 of the CGST Rules, 2017.

The manner of distribution of ITC is governed by:

- Section 20 of the CGST Act.

Due Date for Filing GSTR-6

GSTR-6 must be filed:

- On or before the 13th day of the month succeeding the relevant tax period.

For example:

- GSTR-6 for April 2026 is due on 13 May 2026.

Details Furnished in GSTR-6

The return generally includes:

- GSTIN and legal name of the ISD

- Inward supply details received from suppliers

- Eligible and ineligible ITC

- Distribution of ITC to branches

- Amendments to earlier returns

- Credit notes and debit notes

- ITC reversals, if applicable

Important Points for Businesses

Distribution Only of Input Services

An ISD can distribute credit only relating to:

- Input services.

ITC relating to goods or capital goods cannot be distributed through the ISD mechanism.

Proportionate Distribution

ITC must be distributed proportionately to branches based on turnover, as prescribed under GST law.

Matching with GSTR-2B

Businesses should reconcile supplier invoices with:

- GSTR-2B and GSTR-6 data,

to avoid ITC mismatches.

Consequences of Non-Compliance

Failure to file GSTR-6 on time may result in:

- Late fees under GST law,

- Interest liability in certain cases,

- ITC reconciliation issues for branches,

- Departmental notices and compliance risks.

Incorrect ITC distribution may also attract reversal and penalty proceedings.

Conclusion

GSTR-6 plays a crucial role in the proper distribution of Input Tax Credit within organisations operating through multiple branches. Businesses registered as Input Service Distributors should ensure timely filing, proper reconciliation, and accurate ITC allocation to maintain GST compliance.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from TAX AVIJIT. Reach out to discuss your requirements.